In the realm of statistics and data analysis, the R-squared statistic, also known as the Coefficient of Determination, stands as a fundamental pillar. It plays a pivotal role in assessing the strength and goodness of fit of regression models, making it an indispensable tool for researchers, analysts, and data scientists across diverse domains.

In this article, we embark on a journey to unravel the intricacies of R-squared. We’ll delve into its conceptual underpinnings, explore its practical applications, and equip you with the knowledge to wield it effectively in your data analysis endeavors. Whether you’re a seasoned statistician or a curious novice, the power of R-squared lies within your grasp, offering insights that can shape your data-driven decisions.

What are Regression models and how do they work?

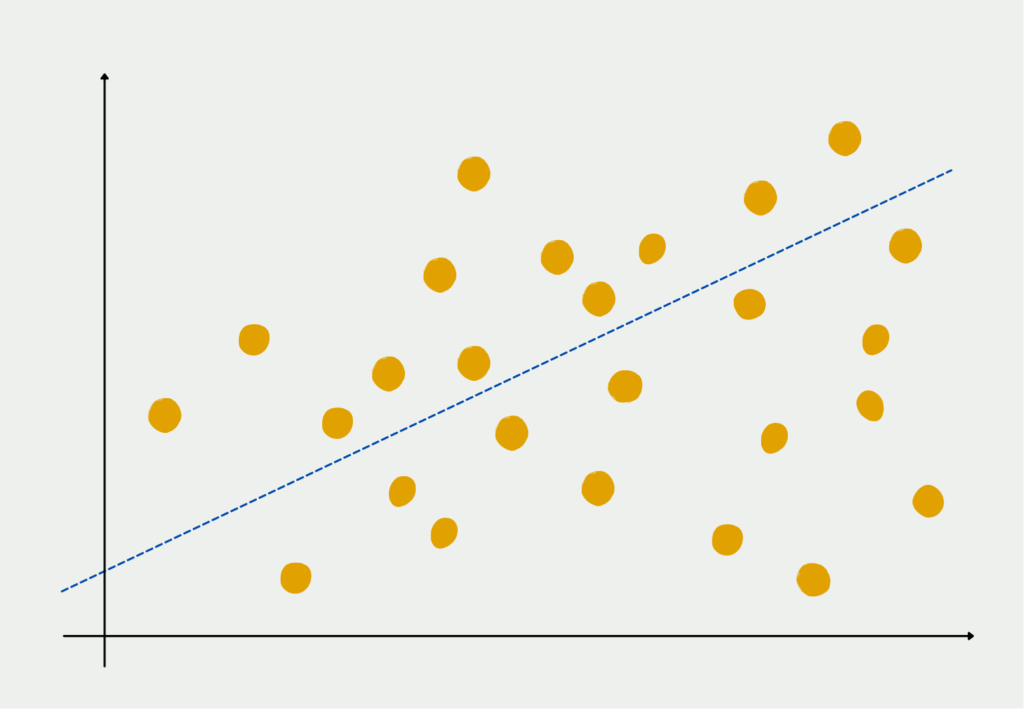

Regression analysis, in its various forms, stands as a cornerstone in the domain of statistics and data analysis. It serves as a versatile tool, bridging the gap between raw data and meaningful insights across a multitude of disciplines, from economics and finance to biology and beyond.

At its essence, a regression model is a mathematical representation of the relationship between one or more independent variables and a dependent variable. It endeavors to uncover and quantify how changes in the independent variables impact the dependent variable. This fundamental concept forms the backbone of both linear and non-linear regression models.

Linear Regression: A Simple Start

Linear regression, the simplest of its kind, explores linear relationships between variables. It assumes that a straight line can aptly capture the connection between the independent and dependent variables. This method has found profound applications in fields such as economics, where it’s used to model the relationship between income and expenditure, or in finance to analyze the association between interest rates and stock prices.

Beyond Linearity: Non-Linear Regression

While linear regression is an invaluable tool, real-world relationships aren’t always linear. Enter non-linear regression, which embraces the complexity of curved relationships. This approach accommodates intricate, non-linear patterns and is employed in areas like biology, where it helps model population growth curves, or in environmental science, to predict the behavior of ecological systems.

Regardless of whether it’s linear or non-linear, the primary aim of regression analysis remains the same: to establish relationships between variables. It serves as a vehicle for unveiling the hidden connections that drive phenomena in diverse domains. In economics, it might reveal how changes in interest rates influence consumer spending. In biology, it can decipher the factors affecting species abundance. In finance, it aids in forecasting stock price movements based on historical data.

What is the Variance and why is it important for R-squared?

Before delving into the depths of R-squared, it’s essential to grasp a fundamental concept that underpins this statistical metric: variance. Variance is the measure of the dispersion or spread of data points around their mean, and it plays a pivotal role in understanding the power and significance of R-squared in regression analysis.

In the context of regression analysis, variance serves as a critical benchmark. It quantifies how data points deviate from the mean or central tendency. This variability in data points is the crux of what regression models aim to capture and explain. In essence, variance reflects the inherent complexity and diversity within the data set.

R-squared, or the Coefficient of Determination hinges on the concept of explained variance. It measures the proportion of the total variance in the dependent variable that is accounted for, or “explained,” by the independent variables in a regression model. In simpler terms, it gauges how well the model captures and clarifies the variability in the data.

The importance of explained variance cannot be overstated. A high value indicates that a substantial portion of the variance in the dependent variable has been successfully accounted for by the model. This implies that the model’s predictions align closely with the observed data, making it a valuable tool for understanding and predicting outcomes.

Conversely, a low R-squared suggests that the model has failed to explain a significant portion of the variance. In such cases, the model may need refinement or additional independent variables to enhance its explanatory power.

As we journey further into the realm of R-squared, it’s crucial to keep in mind that variance lies at the core of this statistic. It illuminates the breadth of possibilities within the data, while R-squared quantifies our ability to navigate and comprehend this variability. Together, they empower data analysts and researchers to evaluate the goodness of fit of regression models and gain deeper insights into the relationships between variables.

How do you calculate the R-squared?

R-squared is a pivotal statistic in regression analysis. It quantifies the goodness of fit of a regression model by measuring the proportion of the variance in the dependent variable that is explained by the independent variables. Calculating it involves a straightforward process that illuminates the model’s ability to capture and clarify the variability within the data.

The Formula for R-Squared

R-squared is computed using the following formula:

\(\) \[ R^2 = 1 – \frac{SSR}{SST} \]

Where:

- SSR (Sum of Squares of Residuals) represents the sum of the squared differences between the actual values and the predicted values by the model.

- SST (Total Sum of Squares) is the sum of the squared differences between the actual values and the mean of the dependent variable.

Step-by-Step Calculation

- Compute the Mean of the Dependent Variable:

\(\) \[ \bar{y} \]

- Calculate the Total Sum of Squares SST by summing the squared differences between each actual value 𝑦𝑖 and the mean:

\(\) \[ SST = \sum_{i=1}^{n} (y_i – \bar{y})^2 \]

- Fit your regression model to the data and obtain the predicted values:

\(\) \[ \hat{y_i} \]

- Calculate the Sum of Squares of Residuals SSR by summing the squared differences between each actual value 𝑦𝑖 and its corresponding predicted value:

\(\) \[ SSR = \sum_{i=1}^{n} (y_i – \hat{y_i})^2 \]

- Finally, apply the formula to compute R-squared:

\(\) \[ R^2 = 1 – \frac{SSR}{SST} \]

How can you interpret the R-squared?

Suppose you are a data analyst working for a real estate agency, and your task is to develop a regression model to predict house prices based on various features like square footage, number of bedrooms, and distance to the city center. After building the model, you obtain an R-squared value of 0.80.

Here’s how to interpret this R-squared value:

- 0.80 R-Squared: This means that your regression model explains 80% of the variability in house prices using the chosen features. In other words, 80% of the fluctuations in house prices are accounted for by factors like square footage, number of bedrooms, and distance to the city center that your model incorporates.

- Good Fit: An R-squared of 0.80 is generally considered a good fit for a regression model. It indicates that your model captures a significant portion of the relationships between the features and house prices.

- Predictive Power: You can have confidence in your model’s predictive power. It suggests that the model’s predictions align well with actual house prices, making it a valuable tool for estimating prices based on the selected variables.

- Room for Improvement: While 0.80 is a strong value, there’s still 20% of the variability in house prices that remains unexplained by your model. This could be due to other factors not included in the model or inherent randomness in the housing market.

- Model Refinement: If achieving a higher R-squared is crucial for your application, you may consider adding more relevant features or refining the model to account for additional sources of variability.

In this scenario, an R-squared value of 0.80 provides confidence in the model’s ability to explain and predict house prices based on the chosen variables. It serves as a valuable indicator of the model’s performance and can guide further steps in model improvement or application.

What are the limitations of R-squared?

While R-squared is a valuable metric for assessing the goodness of fit of a regression model, it has certain limitations and should be used in conjunction with other evaluation measures for a more comprehensive analysis. Here are some key limitations to consider:

- Dependence on Model Complexity: R-squared tends to increase as you add more independent variables to a model, even if those variables are not genuinely improving the model’s predictive power. This can lead to overfitting, where the model fits the training data well but performs poorly on unseen data.

- No Information on Causality: It measures the strength of the relationship between the independent variables and the dependent variable but does not establish causality. A high R-squared does not imply that one variable causes changes in the other.

- Sensitive to Outliers: It is sensitive to outliers, especially in small datasets. A single outlier can significantly impact the value of R-squared, potentially leading to misleading conclusions about the model’s fit.

- Assumes Linearity: The measure assumes a linear relationship between the independent and dependent variables. If the relationship is nonlinear, it may not accurately reflect the model’s performance.

- Multicollinearity: In cases of high multicollinearity (correlation between independent variables), R-squared may overestimate the strength of individual variables’ effects, making it challenging to identify the true contribution of each variable.

- Doesn’t Provide Model Adequacy: R-squared alone does not assess whether the regression model is adequately specified. It does not confirm that the chosen independent variables are the most appropriate for explaining the dependent variable.

- Context Dependency: The interpretation of R-squared varies depending on the specific problem and context. What is considered a “good” value can differ across fields and applications.

- Incompatible for Comparing Models: When comparing models with different dependent variables, R-squared cannot be directly used. It’s essential to consider adjusted R-squared or other appropriate metrics for meaningful comparisons.

- Sample Dependency: R-squared can be influenced by the sample size. In small samples, the value may be less reliable and may not generalize well to larger populations.

- External Factors: It may not account for external factors or changes in the data environment that can affect the dependent variable. These factors may not be captured by the model.

To address these limitations, it’s advisable to complement R-squared with other evaluation metrics, such as adjusted R-squared, root mean squared error (RMSE), or domain-specific metrics. A comprehensive evaluation helps ensure a more accurate assessment of a regression model’s performance and reliability.

What is the adjusted R-squared?

In regression analysis, the adjusted R-squared is a modified version of the traditional R-squared metric. It addresses a limitation of the standard metric by taking into account the number of predictors (independent variables) in the model.

1. Accounting for Model Complexity:

- Traditional R-Squared: It measures the proportion of the variance in the dependent variable that is explained by the independent variables in a regression model. However, as you add more predictors to a model, the R-squared tends to increase, even if those additional predictors do not significantly improve the model’s predictive power. This can lead to overfitting, where the model fits the training data very well but performs poorly on new, unseen data.

- Adjusted R-Squared: To address this issue, the adjusted R-squared adjusts the value based on the number of predictors in the model and the sample size. It penalizes the inclusion of unnecessary predictors that do not contribute meaningfully to the model’s performance. This adjustment helps prevent overfitting and provides a more accurate representation of the model’s goodness of fit.

2. The Formula for Adjusted R-Squared:

The formula is as follows:

\(\) \[ R^2_{\text{adj}} = 1 – \left( \frac{(1 – R^2) \cdot (n – 1)}{n – k – 1} \right) \]

Where:

- n is the number of observations (sample size).

- k is the number of independent variables (predictors) in the model.

3. Interpretation:

- An adjusted R-squared close to 1 indicates that the model explains a significant portion of the variance in the dependent variable while considering the complexity of the model.

- As you add more meaningful predictors to the model, the adjusted R-squared will increase. However, adding irrelevant predictors or those with weak relationships may lead to a decrease in the value.

4. Use in Model Selection:

- Adjusted R-squared is a valuable tool for model selection. When comparing multiple regression models, you can use the adjusted R-squared to identify the model that strikes a balance between goodness of fit and model simplicity.

- Generally, a higher value indicates a better-fitting model, but you should also consider the number of predictors and the practical significance of the model.

In summary, the adjusted R-squared is a modification of the traditional R-squared that considers model complexity. It helps prevent overfitting by penalizing the inclusion of unnecessary predictors. When evaluating regression models or selecting the most appropriate one, the adjusted R-squared provides a more balanced measure of goodness of fit.

This is what you should take with you

- R-squared is a crucial metric in regression analysis that quantifies the proportion of variance explained by independent variables in a model.

- It helps assess whether the relationships between predictors and the dependent variable are statistically significant.

- The R-squared facilitates the comparison of different models and serves as a basis for model selection.

- While valuable, it has limitations, such as sensitivity to model complexity and the inability to establish causation.

- To address these limitations, adjusted R-squared adjusts for model complexity, making it a more robust choice for model evaluation.

- Achieving a high R-squared should not come at the cost of model complexity. Balancing model goodness of fit with model simplicity is essential.

What is the F-Statistic?

Explore the F-statistic: Its Meaning, Calculation, and Applications in Statistics. Learn to Assess Group Differences.

What is Gibbs Sampling?

Explore Gibbs sampling: Learn its applications, implementation, and how it's used in real-world data analysis.

What is a Bias?

Unveiling Bias: Exploring its Impact and Mitigating Measures. Understand, recognize, and address bias in this insightful guide.

What is the Variance?

Explore variance's role in statistics and data analysis. Understand how it measures data dispersion.

What is the Kullback-Leibler Divergence?

Explore Kullback-Leibler Divergence, a vital metric in information theory and machine learning, and its applications.

What is the Maximum Likelihood Estimation?

Unlocking insights: Understand Maximum Likelihood Estimation (MLE), a potent statistical tool for parameter estimation and data modeling.

Other Articles on the Topic of R-squared

The University of Newcastle provides an interesting article on the topic that you can find here.

Niklas Lang

I have been working as a machine learning engineer and software developer since 2020 and am passionate about the world of data, algorithms and software development. In addition to my work in the field, I teach at several German universities, including the IU International University of Applied Sciences and the Baden-Württemberg Cooperative State University, in the fields of data science, mathematics and business analytics.

My goal is to present complex topics such as statistics and machine learning in a way that makes them not only understandable, but also exciting and tangible. I combine practical experience from industry with sound theoretical foundations to prepare my students in the best possible way for the challenges of the data world.